Copper Basic Statistics

Last updated: 2025-02-24

Compiled from USGS MCS 2026 and selected public supplements. Domestic U.S.-only notes are excluded where possible.

1. Highlights & Overview

- World production (2025) is approximately 23,000 kt.

- Global reserves are approximately 980,000 kt.

- The largest producer is Chile, accounting for about 23.0% of global output.

- In 2025, Chile ranked among the top producers (5,300).

- The top 3 countries account for about 48.7% of global output, indicating concentrated supply.

- Source: USGS MCS 原文PDF

- Source: Australia REQ Dec 2025 (PDF)

- Source: Australia REQ Dec 2025 Forecast data (xlsx)

- Source: Australia REQ Dec 2025 Historical data (xlsx)

- Source: ICSG World Copper Factbook 2025

2. Price Trends & Global Market (Events, Trends, and Issues)

- In 2025, production of copper was affected by concentrator shutdowns and lower ore grades at multiple mines in the United States.

- Domestic output of refined copper decreased by an estimated 9% compared with that in 2024 owing to planned maintenance of both primary smelters.

- As of September, copper production started in 2025 at a new mine in Arizona, at a new secondary smelter in Georgia, and at a new secondary refinery in Kentucky.

- By yearend, one additional mine in Arizona was expected to begin commercial operations.

Usage Mix (Based on Public Data)

3. World Mine Production and Reserves

Top Producing Countries(2025, Top 5)

Top Reserves (Top 5)

| Country | Production(2025) | Reserves |

|---|---|---|

| Chile | 5,300 | 180,000 |

| Congo (Kinshasa) | 3,200 | 80,000 |

| Peru | 2,700 | 85,000 |

| China | 1,800 | 41,000 |

| Russia | 1,300 | 80,000 |

| United States | 1,000 | 47,000 |

| Zambia | 940 | 21,000 |

| Australia | 730 | 100,000 |

| Indonesia | 710 | 21,000 |

| Kazakhstan | 710 | 20,000 |

| Mexico | 690 | 53,000 |

| Canada | 500 | 7,000 |

Unit: 千トン

4. Supply-Demand Balance Trend

Unit: kt / Positive values indicate supply surplus; negative values indicate supply deficit.

5. Metallurgical & Physical Properties and Industrial Uses

Copper (Cu) is a transition metal with a face-centered cubic (FCC) crystal structure and is one of the oldest metals utilized by humanity. Industrially, its most important characteristic is its high electrical and thermal conductivity, which ranks second among all metals, just behind silver [40]. Because silver is expensive and not cost-effective for large-scale infrastructure, copper essentially acts as the "skeleton supporting the electrification of the world" [40].

Pure copper is extremely soft and highly ductile and malleable, making it easy to plastically deform into diverse shapes—ranging from ultra-fine wires (magnet wire) to intricately shaped heat exchanger piping [41]. Additionally, when exposed to the atmosphere, it forms a dense oxide film (like verdigris) on its surface that prevents internal corrosion, providing it with excellent corrosion resistance in both freshwater and seawater environments [41]. Furthermore, similar to silver, copper ions exhibit a potent antibacterial and sterilizing effect (oligodynamic effect) that destroys bacterial cell walls; as a result, it is highly valued for applications requiring hygienic environments, such as hospital doorknobs and HVAC systems [41].

Its traditional major industrial applications have centered around power infrastructure and construction demand, including the power grids (infrastructure) connecting power plants to individual homes, indoor wiring for buildings, communication cables, transformers, and the windings inside various motors [40]. Even in the projected end-use consumption breakdown for 2025, its usage is broadly distributed across construction, infrastructure (power and telecommunications), transportation, industrial equipment, and consumer/general products.

However, copper is now hailed as the "new oil of the 21st century," making it the most critical metal for physically realizing the green Energy Transition [40]. Electric vehicles (EVs), owing to their massive drive motors and high-capacity battery wiring, consume approximately three to four times more copper than traditional internal combustion engine vehicles. Moreover, an enormous amount of copper is indispensable for wiring photovoltaic (PV) solar panels, laying submarine cables for offshore wind farms, and constructing massive smart grids to distribute renewable energy across wide areas [40]. As noted in reports by Goldman Sachs, complete decarbonization is simply impossible without copper acting as the physical medium [40].

6. Structural Issues Governing Supply and Demand

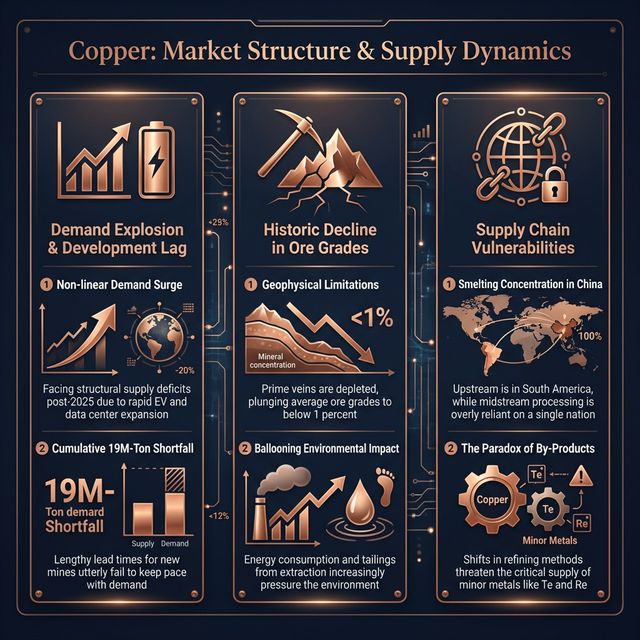

The supply-demand structure for copper is clutching a ticking time bomb of an impending, massive "supply shortfall."

The first special circumstance is the "nonlinear explosion of demand" driven by decarbonization, coupled with a "delay in mine development" that is failing to keep pace. According to forecasts by BloombergNEF, surging demand from EVs, energy storage, and data centers will push the copper market into a structural deficit as early as 2025 and beyond. It warns that unless the development of new mines and recycling facilities progresses at a rapid pace, a cumulative supply shortfall of 19 million tons will occur by 2050 [44]. While global production for 2025 is estimated at around 23,000 kilotons, the expansion of existing mines alone is insufficient to adequately respond to this skyrocketing demand.

Lying at the root of these supply constraints is the second circumstance: the geophysical limit known as the "historic decline of ore grades" [43]. The grade (copper content percentage) of copper ores mined in the past was several percent, but due to the depletion of prime veins, the average grade of porphyry copper deposits and others currently being mined has dropped to below 1%. This means that to obtain the same 1 ton of refined copper, miners must extract, crush, and chemically process several to dozens of times more rock than in the past. As a result, the energy consumption (fossil fuels) associated with ore processing, water resource consumption, and the discharge of toxic waste rock (tailings) are increasing exponentially [40]. The industry is confronted with an "environmental dilemma" in which the very process of producing the metals needed to build a green society is, ironically, escalating environmental burdens and carbon emissions [40].

The third special circumstance involves the complex supply chain structure of the refining process and its by-products. As evidenced by the top three countries (Chile, the Democratic Republic of the Congo, and Peru) accounting for nearly 48.7% of world production, mine production (the upstream) is heavily concentrated in South America and Africa. However, the "smelting and refining" processes (the midstream)—which extract pure copper from the mined copper concentrates—are excessively concentrated in China [44]. By expanding its smelting capacity as a national strategy, China is establishing itself as a "price maker" that holds the choke points of the global value chain [45]. Although Western nations are rushing to reshore supply chains (friend-shoring) from the perspective of economic security, the construction of new copper smelters—which entail enormous environmental impacts—is exceptionally difficult due to stringent environmental assessments and the opposition of local residents [44].

Furthermore, the "by-product paradox" inherent within the copper refining process itself cannot be overlooked. Minor metals indispensable to modern high-tech industries—such as tellurium (Te) and selenium (Se) required for solar panels (CdTe thin-film cells), and rhenium (Re) needed for superalloys—do not have standalone mineral deposits. Almost all of them are recovered from the by-products (anode slimes and dust in exhaust gases) generated during the pyrometallurgical and electrolytic refining process of copper [46]. In recent years, as a response to lower grade ores, the ratio of hydrometallurgy (the SX-EW method)—which dissolves copper using chemicals without the use of a blast furnace—has increased, but this method cannot recover tellurium or selenium [13]. A highly complex and fragile dependency lurks within the copper value chain, where a shift in copper production technology could suddenly sever the supply of critical metals for seemingly unrelated next-generation clean energy technologies [13].

References

- [13] (PDF) The Evolving Copper‐Tellurium Byproduct System: A Review of Changing Production Techniques & Their Implications - ResearchGate

- [40] Copper as a Critical Resource in the Energy Transition - MDPI

- [41] Mechanical, Electrical, and Thermal Characterization of Pure \... - MDPI

- [43] The role of copper in the energy transition - DNV

- [44] Supply Chains Struggle as Energy Transition Drives Surging Demand for Metals: BloombergNEF Finds

- [45] (PDF) Copper as a Critical Resource in the Energy Transition - ResearchGate

- [46] Recovery of rhenium, a strategic metal, from copper smelting effluent - ResearchGate